Happy’s Tech Talk #28: The Power Mesh Architecture for PCBs

Happy’s Tech Talk #28: The Power Mesh Architecture for PCBs It’s Only Common Sense: Would You Join Your Own Company?

It’s Only Common Sense: Would You Join Your Own Company? The Chemical Connection: Reducing Etch System Water Usage, Part 2

The Chemical Connection: Reducing Etch System Water Usage, Part 2Asia/Pacific Semiconductor Fabless Market Size Decline 6.5% YoY in 2022, Expected Steady Growth in 2024

May 17, 2023 | IDCEstimated reading time: 2 minutes

According to the IDC Worldwide Semiconductor Technology Supply Chain Intelligence: IDMs, Fabless, Foundry, OSAT and Materials, factors including the Ukraine-Russia war, Chinese lockdowns, high inflationary pressures, and demand fluctuations resulted in the Asia/Pacific region’s semiconductor fabless market losing growth momentum in 2022 and an end to the trend of rising Integrated Circuit (IC) prices. The region’s semiconductor fabless market size in 2022 was US$78.5 billion, a decline of 6.5% compared to 2021 which marks the first year-on-year negative growth performance since the onset of the pandemic.

The global semiconductor industry experienced a sharp decline in 2022 after seeing growth in 2020 and 2021. Demand for consumer electronics including smartphones, laptops, tablets, TVs, and monitors plummeted while supply chain inventory levels increased. Short-term supply began exceeding demand, forcing companies to slow down the pace of expansion.

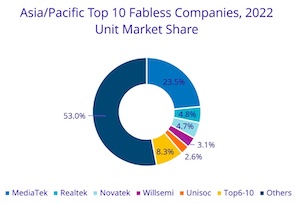

“The annual growth rate of the top 10 companies in Asia/Pacific was -5.1%, which was better than the overall market performance. From the perspective of regional momentum, Taiwan leads with 73% market share, while China and South Korea holds 22% and 5% market share respectively. Having the highest market share, Taiwan is considered to have a wide and deep influence on the region’s fabless market,” said Galen Zeng, Senior Research Manager, Semiconductor Research, IDC Asia/Pacific.

Among the top 10 semiconductor technology vendors are Taiwan’s MediaTek, Realtek, Novatek, and Himax; China’s Willsemi, Unisoc, HiSilicon, GigaDevice, and Bitmain; and South Korea’s LX Semicon. MediaTek plays an influential role with a market share of nearly 50% among the top 10 companies. The growth of MediaTek played a leading role by helping make up for the shortfalls of other Taiwanese firms, resulting in a 2% increase in Taiwan’s semiconductor fabless market share in the region compared to 2021. Chinese companies were affected by the overall unfavorable environment in China and saw their market share decline by 2%, while South Korea’s market share did not experience any major changes.

As for the outlook for 2023, although products such as display driver ICs and touch and display driver ICs were the first to enter a down cycle, these are now seeing the light of day with several products starting to see urgent orders and the need for inventory replenishment. The market demand for most semiconductor ICs remains depressed and the market size outlook remains sluggish. During the high base period in the first half of 2022, it was anticipated that the region’s fabless market size in the first half of 2023 would decrease by over 20% year-on-year, supply chains would continue to actively control inventory, and fabless companies would maintain low wafer production volumes at foundries. During the second half of 2023, it is expected that inventory will return to a healthy level, and that demand will also slowly recover. IDC forecasts that the Asia/Pacific region’s semiconductor fabless market size will decline by 19.1% year-on-year in 2023. It also predicts that it will progressively show stable and steady growth in 2024 as companies gradually shift products to applications including AI, high-performance computing, servers, data centers, automotive electronics, and industrial electronics to diversify operational risks.

This IDC research, Worldwide Semiconductor Technology Supply Chain Intelligence: IDMs, Fabless, Foundry, OSAT and Materials, provides holistic analysis of the worldwide semiconductor supply chain industry. The program delivers comprehensive insights across supply chain including materials, Fabless, OSAT, and semiconductor equipment. It covers the analysis of market dynamics, market competition, and key vendors' activities and the strategy plans to understand the key trends and factors impacting the market as it transitions to the new world of digital competition under geopolitical impact across countries and companies.

Share on:

Suggested Items

IDTechEx Discusses Low-Loss Materials: The Enabler of Future Connected Vehicles?

05/06/2024 | IDTechExFuture connected vehicles will offer future drivers a safer, smoother, and more convenient driving experience. Not only will drivers get access to more navigation and entertainment options, but they will also gain access to safety technologies that will potentially reduce accidents, improve congestion, and reduce emissions globally by allowing vehicle safety systems to communicate with each other and with city traffic infrastructure.

HBM Prices to Increase by 5–10% in 2025, Accounting for Over 30% of Total DRAM Value

05/06/2024 | TrendForceAvril Wu, TrendForce Senior Research Vice President, reports that the HBM market is poised for robust growth, driven by significant pricing premiums and increased capacity needs for AI chips.

Tablet Shipments Show Signs of Recovery in Q1 2024

05/06/2024 | IDCAfter more than two years of decline, worldwide tablet shipments posted modest year-over-year growth of 0.5% in the first quarter of 2024 (1Q24), totaling 30.8 million units, according to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker.

Industrial PC Market Size to Record $1.75 Billion Growth from 2023-2027

05/03/2024 | PRNewswireThe global industrial pc market size is estimated to grow by USD 1.75 billion from 2023 to 2027, according to Technavio. This growth is expected to occur at a Compound Annual Growth Rate (CAGR) of almost 6.29% during the forecast period.

Real Time with… IPC APEX EXPO 2024: Direct Imaging Equipment and Quad-wave DLP Light Engine Technology

05/03/2024 | Real Time with...IPC APEX EXPOGuest Editor Kelly Dack and MivaTek's Brendan Hogan delve into the company's innovative technologies, including direct imaging equipment and quad-wave DLP light engine technology. They highlight the benefits of direct imaging, compensation, and DART technology.